Table of Contents

halbergman/iStock via Getty Images

Agricultural Sentiment Remains Bullish

Sanctions continue to come down on Russia and Belarus, shedding a bigger spotlight on the crop nutrient and food crisis. Europe is feeling the most effects, while potash and nitrogen-producing companies like our stock picks gear up for the gains. Commodities continue to run hot because they are in short supply across the globe and companies that produce and process them are in demand and an excellent hedge against inflation. With this in mind, the market has sunk almost all ships this week. Now that potash exports from Russia and Belarus are restricted, U.S. producers are exploring debottlenecking initiatives by improving efficiencies and operations, to ramp up crop nutrient production. During the recent Q1 2022 Earnings Call, Mosaic President & CEO Joc O’Rourke said it best:

“Realized prices in the second quarter are expected to be $40 to $60 per tonne higher than realized prices in the first quarter. We are actively increasing productive capacity in our potash business. We’re already running assets at a 10.8 million tonne run rate with the ramp-up of K3 and running Colonsay at 1.3 million tonnes per annum. As we move forward, we have project teams actively working on two additional miners for Esterhazy, the de-bottlenecking of the Esterhazy mill, and the restart of the second Colonsay mill.”

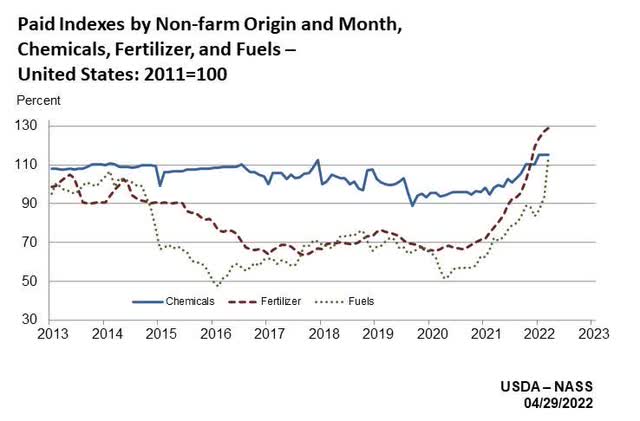

As sanctions in Europe are potentially changing trading patterns, customers are seeking companies with more reliable supplies. As I wrote in You Name It, We’re Out Of It, shortages in agricultural products among other commodities are key drivers of the rising prices. Natural gas is a key raw material and main fuel source used in the ammonia production of nitrogen. With spiking natural gas prices across Europe, the price of nitrogen is increasing, so there’s still plenty of time to capitalize on the price action involving fertilizers and agricultural chemicals like nitrogen and potash. In fact, according to the National Agricultural Statistic Service chart below, agricultural chemicals and fertilizers are outperforming fuels and as long as demand exceeds supplies, our three stocks are an excellent hedge against inflation and consideration for portfolios.

Chemicals, Fertilizers, and Fuels Indexes (USDA – NASS)

3 Best Agricultural Stocks To Buy

Since February, increasing prices for potash and mixed fertilizers are creeping higher, and as we look at the chart above, showcasing the significant surge in fertilizers, it paints a clear picture of why our stock picks are centered around this industry. These businesses are in very good shape, have excellent profitability, and are set to pass along rising costs to consumers – making them excellent stocks to help inflation-proof portfolios. Agriculture stocks are in a bull market and these three recommendations up year-to-date (IPI- 59%, MOS- 61%, CF- 42%) continue to offer an excellent valuation framework and are supported by strong organic growth demand.

1. Intrepid Potash, Inc. (NYSE:IPI)

-

Market Capitalization: $966.74M

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/5): 1 out of 262

-

Quant Industry Ranking (as of 5/5): 1 out of 13

-

Analysts’ Upward Earnings Estimate Revisions: 3

The skyrocketing price of fertilizers and agricultural chemicals increases concerns about food shortages. Meanwhile, companies like Intrepid Potash (IPI) are reaping the financial rewards. Based in Denver, Colorado, this fertilizer manufacturer is one of the largest producers of potassium chloride, specializing in the potassium-rich salt a.k.a. potash mined from seabed. This product helps to support crop yields and enhance water preservation. With its subsidiaries, IPI engages in potash extraction and production globally. Last week, Intrepid Potash topped Q1 earnings and revenue estimates. IPI is trading higher as profits are bolstered following sanctions limiting potash shipments from Russia and Belarus.

The stock has been trending upward with a +60% YTD increase, and over the last year, it’s seen a +100% share price jump. IPI’s overall Valuation grade is B+ and indicates this stock is trading at a discount, with current P/E ratios of 3.95x, more than 75% below its sector peers.

IPI Factor Grades (Seeking Alpha Premium)

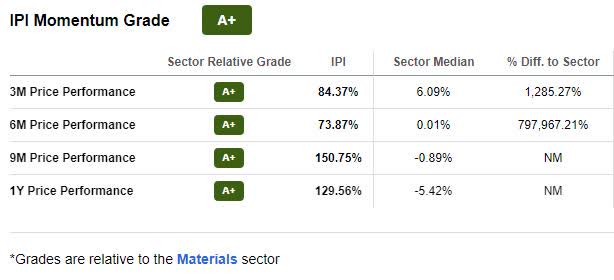

As we take a closer look at IPI’s collective factor grades, momentum is stellar, and we believe the stock overall is bullish.

IPI Momentum Grade

Intrepid’s momentum is beyond impressive, especially over its 6M Price Performance, with a 797,967% difference to the sector.

IPI Momentum Grade (Seeking Alpha Premium)

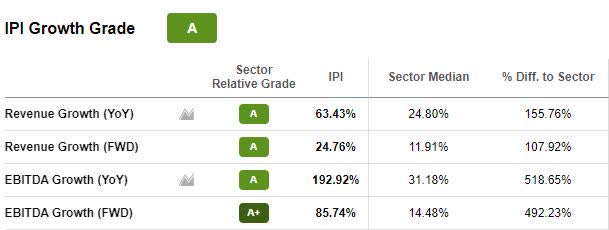

IPI has improved its financial situation by increasing its top and bottom lines. IPI still ranks #1 in its industry and sector, and as I wrote in my article titled Best Commodity Stocks to Buy Now: Top 5 For 2022, “Intrepid is growing with a favorable outlook, zero debt on its balance sheet, and a $35M share buyback announcement, so let’s explore the growth and profitability numbers.” As evidenced by the momentum grades, we believe there’s plenty of room in the future for continued growth and profitability.

IPI Growth & Profitability

Despite IPI contemplating bankruptcy a few years ago, the stock has rebounded nicely after its $35M revolving credit agreement removed concerns. IPI has focused on the future, paying off handsomely, as showcased in its A Growth Grade.

IPI Growth Grade (Seeking Alpha Premium)

According to Seeking Alpha Contributor Jason Wong, “In 2020, the sales price per ton of IPI potash was $250.” Fertilizers are setting price records, with a current average price for potash at $875/ton.

Intrepid announced Q1 2022 Earnings last week, and both top- and bottom-line beat. EPS of $2.32 beat by $0.09, and revenue of $94.16M beat by $3.29M (58.56% YoY). With year-over-year revenue growth above 58%, forward operating cash flow growth +351%, and a growing balance sheet, it’s no wonder company executives are optimistic for 2022 and beyond, given the current landscape.

“The trend of high prices certainly across most fertilizer products continue, and we deliver an average net realized price, which was $703 per ton for potash and $469 per ton for Trio, which represent respective increases of approximately 150% — and 100% compared to the first quarter of 2021. In our potash segment, our Q1 sales totaled just over $56 million, a 30% increase compared to the prior-year quarter, and gross margin totaled $29 million. In our Trio segment, our sales totaled $41 million, a roughly 73% increase compared to the prior-year quarter, and gross margin totaled $16.1 million,” said Bob Jornayvaz, Intrepid Co-Founder & CEO, during the Q1 2022 Earnings Call.

Fertilizers and agricultural chemicals benefit from the current market environment, so we’re highlighting another potash producer that’s been headlining news.

2. The Mosaic Company (NYSE:MOS)

-

Market Capitalization: $22.59B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/5): 2 out of 262

-

Quant Industry Ranking (as of 5/5): 2 out of 13

-

Analysts’ Upward Earnings Estimate Revisions: 19

Like IPI, The Mosaic Company (MOS), through its subsidiaries, markets potash and phosphate nutrients globally. MOS is capitalizing on the sanctions imposed on Russia and Belarus, causing MOS to benefit from the demand. All forms of fertilizers and agricultural nutrients are in short supply. As MOS looks to ramp up its production, companies like MOS, IPI, and our next stock pick CF are shattering records in the fertilizer industry. As a Seeking Alpha report highlights,

“‘Russia is a major, major exporter across all of the major fertilizers… losing Russian exports is a very big deal,’ says Josh Linville of StoneX Group, noting that the country accounts for 14% of urea, as much as 31% of UAN, 10% of phosphate, and nearly 20% of the global operating potash capacity.”

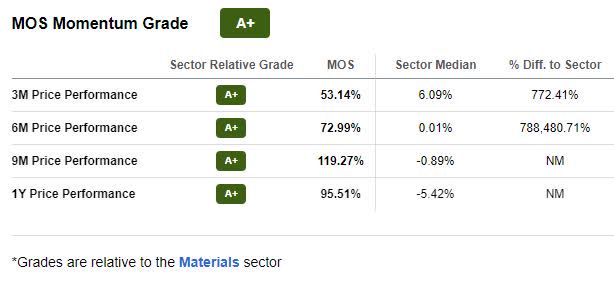

Mosaic’s C Valuation is fair, with a forward P/E ratio of 4.92x, nearly 60% below its sector peers, and forward EV/Sales of 1.29x, more than 20% below the sector, indicating this stock comes at a relative discount. Additionally, MOS has an excellent runway and great momentum. MOS is trading under $65/share with stellar short-term price performance. Looking at the A+ Momentum grade below, this stock is a top stock in its respective sector, gradually outperforming its peers on a quarterly price-performance basis.

MOS Momentum (Seeking Alpha Premium)

On a bullish trend, as we look to MOS’s future, consider its incredible growth and profitability.

MOS Growth And Profitability

We cannot stress enough that agricultural prices are at multi-year highs with zero slowing of demand in sight. As the need for crop nutrients are in high demand to try and account for crop shortages stemming from geopolitical issues in Europe, fertilizer stocks like MOS will advance. SA Contributor Michael Wiggins De Oliveira writes in his article Mosaic Q1 Earnings: Ramps Up Capital Returns, Expect 17% Yield:

“The most important takeaway here is that there is no indication that revenues are going to slow down. Yes, Q1 2022 had the easiest comparison for Mosaic, against Q1 of last year, and for the remainder of the year, the comparisons are slightly more challenging. But at the same time, you have to remember that the main catalyst that got us here, namely the invasion of Ukraine and related events, only started to play out in the later parts of Q1. That means that Mosaic’s strongest revenues are still to come in the upcoming quarters.”

MOS Growth Grade (Seeking Alpha Premium)

Year-over-year revenue growth is 52.30% compared to 24.80% for the sector. Year-over-year EBIT Growth trumps its median peers by 816.96%.

MOS Profitability Grade (Seeking Alpha Premium)

MOS has substantial cash from operations, with $2.37B. Continued demand for potash should only create more upside in the profitability figures and reemphasize its financial performance.

MOS recently announced its Q1 2022 performance. Although both top- and bottom-lines were amiss, with EPS of $2.41 missing by $0.01 and revenue of $3.92B missing by $125.99M (70.75% YoY), MOS should continue to see business boom given the favorable market backdrop.

“Phosphate segment adjusted EBITDA totaled $632 million, reflecting the impact of strong pricing, which more than offset higher input costs. Potash also benefited from higher prices, as well as the transition to Esterhazy K3, and the elimination of brine inflow management costs. As a result, segment adjusted EBITDA totaled $651 million…Looking forward, we continue to see agricultural market strength extending well beyond 2022,” said O’Rourke.

As the strength in agricultural prices continues to climb, coupled with fertilizer supply constraints creating a rise in nutrient prices, fertilizer stocks will continue to benefit, as we also see in our next stock pick, CF Industries Holdings, Inc.

3. CF Industries Holdings, Inc. (NYSE:CF)

-

Market Capitalization: $20.17B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/5): 8 out of 262

-

Quant Industry Ranking (as of 5/5): 4 out of 13

-

Analysts’ Upward Earnings Estimate Revisions: 14

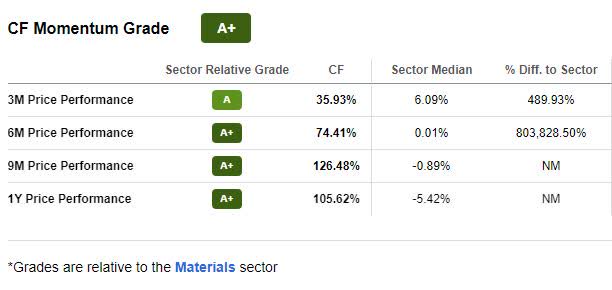

Primarily serving cooperatives and independent fertilizer distributors and companies, CF Industries Holdings, Inc. (CF) manufactures and sells hydrogen and nitrogen products for energy and fertilizer companies. On a notable upward trend since Q4 of 2021, CF has a YTD price increase of +40%, and over one year is up +100%. Currently, the stock is trading just under $100/share with stellar momentum. With A’s over the last four quarters and six-month price performance relative to its sector peers that’s unheard of, as evidenced below, it’s no wonder this stock is a strong buy.

CF Momentum Grade (Seeking Alpha Premium)

Although CF possesses a D valuation grade, with momentum expected to continue and tailwinds supported by solid demand and pricing fundamentals for fertilizers backed by substantial growth and profitability metrics, we believe the future outlook for CF is strong.

CF Growth & Profitability

CF has 14 FY1 Up analyst revisions within the last 90 days and zero downward revisions despite recent earnings being amiss. Q1 2022 revenue of $2.87B beat by $246.02M, an increase of 173.66% year-over-year, so the company is optimistic about its long-term free cash flow, which is excellent, up 238.28% compared to its sector.

With strong overall growth and profitability metrics, CF plans to increase the ratable portion of its share repurchase program to position itself to return more than $1B to shareholders on an annualized basis. CF reached its long-term gross debt target of $3B in 2022 and plans to maintain its CAPEX range of $500M to $550M per year, including expenses around maintenance and clean energy initiatives.

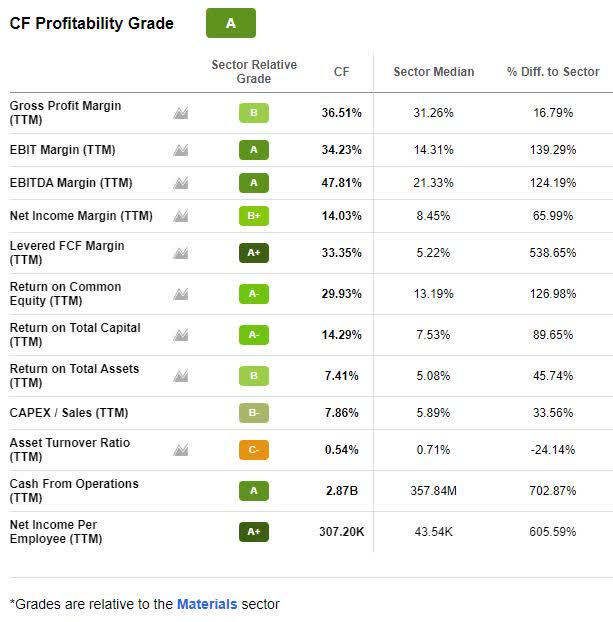

The overall SA Profitability grade for CF is A. From Gross Profit to Net Income Per Employee, there are solid profitability grades for this stock. SA Author Leo Nelissen digs down deep and highlights, “CF Industries has the ability to boost production, benefit from high(er) margins, and generate strong double-digit free cash flow yield used to buy back shares.”

CF Profitability Grade (Seeking Alpha Premium)

CF is a U.S.-based company.

“Natural gas accounts for approximately 40% of total production costs for nitrogen products, if gas prices increase in Europe, that means competitors will have to increase the prices of nitrogen products. Consequently, in the US, CF Industries will also be able to raise its own costs, without having to meaningfully increase its input costs. This is going to lead to a bounty for shareholders,” writes Michael Wiggins De Oliveira, Seeking Alpha Marketplace Author.

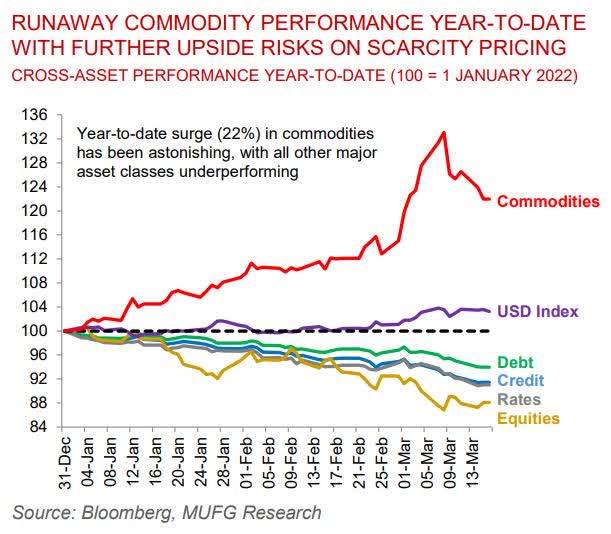

Globally, people are suffering from food shortages, increasing demand, supply chain disruptions, and runaway energy and commodity prices. Commodities and in this case agriculture are experiencing a bull market. Year-to-date commodity performance is astounding, as showcased by the below chart.

Commodity Performance (Dec 2021 to Mar 13, 2022) (Bloomberg, MUFG Research)

Fertilizers are in short supply, with 28% of fertilizers made from nitrogen coming from Russia and Ukraine, creating a surge that makes these stocks excellent hedges against rising inflation and fundamentally sound.

Conclusion

Inflation, war, and agricultural market trends are increasing demand and boosting fertilizer and crop prices. According to the largest asset manager in the world and Seeking Alpha Contributor BlackRock, on average since 1997, commodities have historically outperformed the S&P 500 in the first 12 months after the beginning of a rate hiking cycle.

“Commodity indexes have rallied amid heightened geopolitical uncertainty and structural supply shortages… commodities have historically shown resiliency in rising rate environments and can help investors hedge against rising inflation and diversify portfolios.”

IPI, MOS, and CF are Strong Buys based on our quant ratings, excellent growth, profitability, and momentum grades. They respectively have forward revenue growth of 24.75%, 24.60%, and 26.77%. Fertilizers and agricultural chemicals are defensive in the current inflationary environment where there is high demand for food, especially amid global shortages. Factor in the costs being passed onto customers, and these commodities are likely to maintain their bullish trend for the foreseeable future.

Our investment research tools help to ensure you’re furnished with the best resources to make informed investment decisions. Check out our list of other Top Materials Stocks, or you can create your own Stock Screen to help you achieve diversification into desired sectors you like.

https://seekingalpha.com/article/4508376-best-agricultural-stocks