Table of Contents

ipopba

World production trade stipulations worsened for a 3rd successive month in November, with the JPMorgan World Production Buying Managers’ Index™ (PMI™), compiled by means of S&P World, shedding from 49.4 in October to 48.8; its lowest stage since June 2020.

The survey’s sub-indices recorded an greater price of lack of manufacturing unit manufacturing which appears to be like set to achieve momentum within the coming months. Order books persevered to weaken at a price some distance outstripping the tempo at which producers are reducing output, which means companies are seeing unparalleled build-ups of unsold inventory. This manufacturing decline has in flip necessitated a marked decline in enter purchasing, a shift to stock discount, and a renewed fall in employment, the latter representing the primary time that manufacturers have lower staffing ranges for 2 years and a very powerful signal of rising retrenchment amongst producers international.

World manufacturing unit output decline speeds up

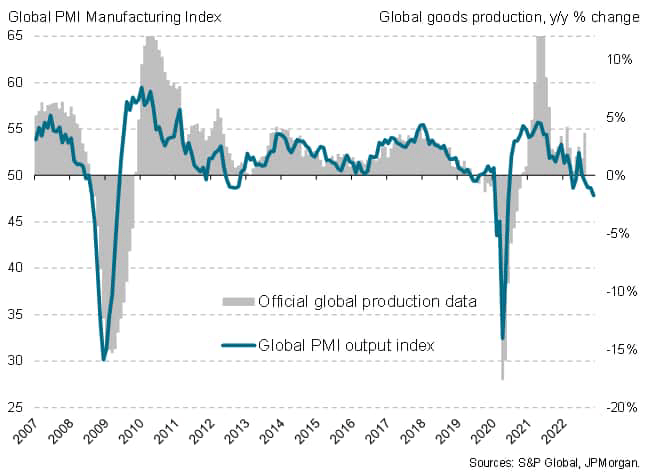

The worldwide production PMI survey’s Output Index, which acts as a competent advance indicator of tangible international output traits, signalled a fourth consecutive per month fall in international manufacturing unit manufacturing in November, with the velocity of decline accelerating to the quickest since June 2020. Except the early months of the pandemic, the most recent decline was once the steepest since Might 2009, right through the worldwide monetary disaster.

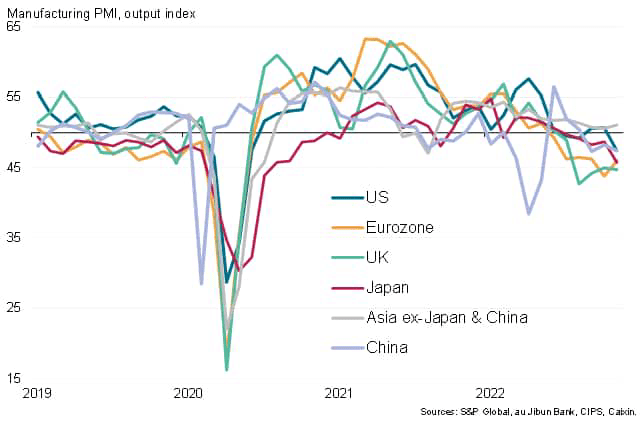

Asia leads production, however traits range markedly around the area

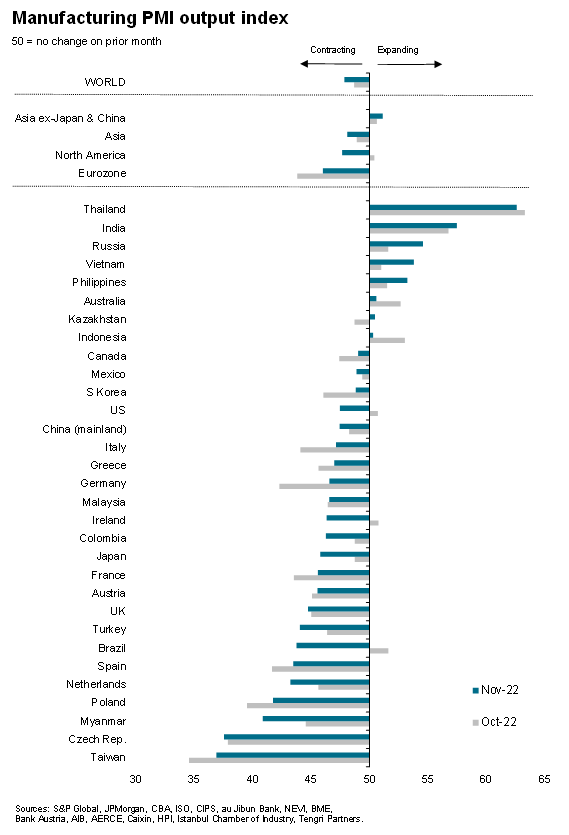

Of the 31 economies for which S&P World PMI information are to be had, most effective 8 reported upper manufacturing volumes in November, down from ten in October, and – of those – most effective marginal expansion was once observed in 3 economies. Thailand reported the most powerful output expansion adopted by means of India, serving to Asia outperform the worldwide financial system, albeit nonetheless declining. 4 of the highest 5 appearing production economies had been present in Asia in November, however each China and Japan noticed greater charges of contraction, the previous hit by means of additional COVID-19-related restrictions.

World production output

Production output in key economies

Output fell for a 3rd successive month in China, with the velocity of decline amassing tempo to finish the worst three-month spell since 2015. COVID-19 restrictions in mainland China additionally confirmed a knock-on impact in Taiwan, which reported the sharpest downturn of all economies surveyed, albeit additionally reeling from a downturn in export call for.

Throughout large areas of the sector, Europe noticed the steepest downturn in production right through November, with a deepening downturn in the United Kingdom contrasting with indicators of the velocity of contraction easing within the eurozone. Firms in Germany particularly benefitted from stepped forward provide stipulations. Each the United Kingdom and eurozone are nonetheless reporting probably the most worst performances observed because the world monetary disaster and 2012 debt disaster respectively.

The USA additionally slipped into contraction, a downturn which – barring the preliminary COVID-19 lockdowns – was once the steepest because the world monetary disaster. Brazil likewise noticed a renewed fall in manufacturing, and production remained in decline throughout Canada and Mexico.

Falling call for

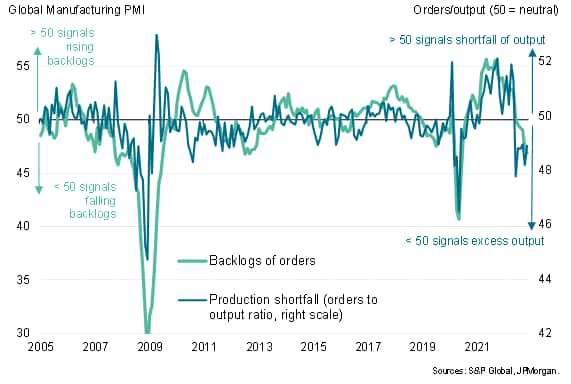

One of the vital key regarding metrics from the PMI surveys in the case of the near-term outlook was once the level to which new orders fell in comparison to manufacturing. New orders had been falling at a significantly quicker tempo than output in contemporary months, in reality, extra temporarily than at any time because the world monetary disaster, barring preliminary pandemic months. This divergence means that, in spite of contemporary manufacturing cuts, producers proceed to function with extra capability relative to present call for.

This dearth of call for was once likewise mirrored in an greater price of decline of backlogs of orders at producers. Those exceptional orders at the moment are additionally falling at a price now not observed since 2012 (with the exception of the downturn observed at first of the pandemic), to trace strongly on the building of extra running capability.

World production order books

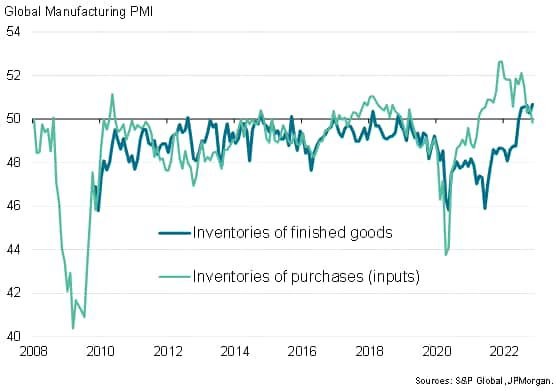

Two being worried stock alerts

The PMI survey’s two gauges of producing inventories in the meantime moved in several instructions, each offering additional being worried alerts at the well being of the manufacturing unit sector.

First, inventories of uncooked subject material inputs fell in November for the primary time since March 2021, as expanding numbers of factories intentionally decreased their enter purchasing for charge concerns in keeping with decreased manufacturing necessities. November’s drop in enter purchasing was once in reality the 5th fastest since similar world information for this sequence had been first to be had in October 2009, exceeded most effective by means of the declines observed right through the preliminary segment of the pandemic in early 2020.

World production inventories

2d, November noticed the biggest build up in inventories of completed items inventory recorded since similar world PMI survey information had been to be had in 2007, representing a 5th consecutive month of strangely prime stock-piling. Whilst some classes can see inventories upward thrust as corporations construct inventory to fulfill sturdy call for in coming months, this has now not been the main issue at the back of the upward push in inventories in contemporary months. As a substitute, and by contrast, the survey has observed a pointy upward thrust in companies reporting upper inventories because of weaker-than-anticipated gross sales.

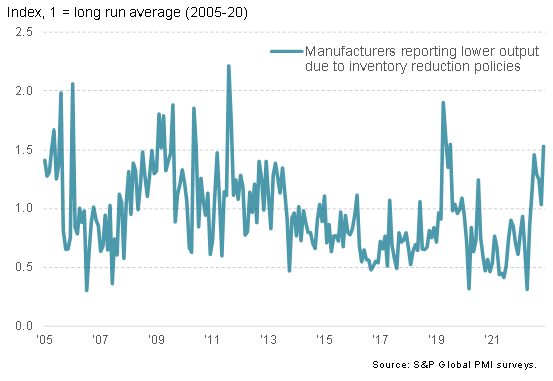

With corporations intentionally decreasing inventories of uncooked fabrics and turning into increasingly more apprehensive concerning the build-up of unsold warehouse post-production inventory, November noticed a commensurate spike upwards within the choice of corporations international reporting that output was once being lower as a part of planned efforts to scale back inventories. This, due to this fact, signifies that the negative affect of falling ultimate call for from consumers is being exacerbated by means of a transfer from stock development to stock discount.

International production output cuts because of stock discount insurance policies

Missing self belief, manufacturers get started reducing employment

Two different survey sub-indices introduced discouraging information at the outlook for production. First, expectancies of output over the 12 months forward remained a number of the lowest recorded since similar information had been to be had in 2012, selecting up moderately from October amid indicators of bettering provide chains and decreased fears over the hot power marketplace disaster, but proceeding to run at a distressed stage.

2d, manufacturers lower headcounts on steadiness in November, incessantly mentioning the loss of call for, issues over extra capability, emerging prices and gloom about long term possibilities. Despite the fact that most effective marginal, the discount in employment was once the primary recorded since October 2020 and probably represents a shift to a extra cost-reduction focal point for world production, which the long run output expectancies index suggests has additional to run.

Long run output expectancies

Editor’s Be aware: The abstract bullets for this text had been selected by means of In search of Alpha editors.

https://seekingalpha.com/article/4562173-global-manufacturing-downturn-intensifies-as-firms-cut-capacity