Table of Contents

Evkaz/iStock by the use of Getty Photographs")

Given the upward thrust in rates of interest that we’ve got observed in recent times, considerations have fastened over any corporate with ties to the development house. Even companies that proceed to submit powerful effects on each the highest and backside traces were sufferers of this marketplace. A super instance of this can also be observed via taking a look at Simpson Production (NYSE:SSD), an undertaking targeted at the design, engineering, and production of wooden and urban building merchandise comparable to believe plates, fasteners, mechanical anchors, adhesives, and extra. Sadly, in contemporary months, stocks of the corporate have no longer handiest adopted the marketplace decrease, however controlled to underperform the marketplace. This comes at a time when income and income are emerging well and when stocks are buying and selling at moderately reasonable ranges. This isn’t to mention that the corporate would possibly not enjoy some ache shifting ahead. However given how reasonable the inventory appears to be like now, it is tricky to consider a practical state of affairs the place stocks can be materially overpriced.

A pleasing play at the building marketplace

Again in March of this 12 months, I wrote a piece of writing that took a moderately impartial stance on Simpson Production. In that article, I chronicled the corporate’s upward thrust, from a income and profitability viewpoint, over the prior few years. I concluded that the company was once a high quality operator within the building fabrics marketplace, however I additionally identified that probably the most enlargement it skilled lately will have been transitory. At the moment, I felt as even though stocks of the corporate had been roughly somewhat valued, main me to price it a ‘grasp’ to replicate my view that stocks will have to roughly fit the returns of the wider marketplace for the foreseeable long run. Since then, the corporate has in fact underperformed the marketplace to some extent. Whilst the S&P 500 is down 13.8%, Simpson Production has generated a loss for traders of 17.3%.

Writer – SEC EDGAR Knowledge

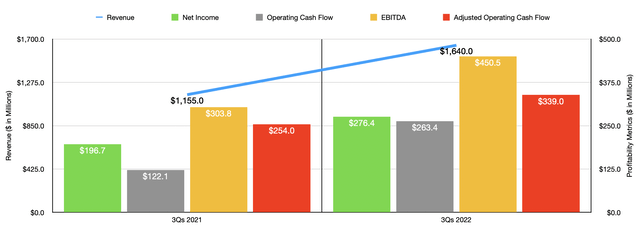

You may assume that if the corporate was once underperforming the marketplace like this, the monetary image of the trade was once appearing indicators of weak point. However that isn’t the case. If anything else, the other is happening. To look what I imply, we’d like handiest quilt effects in the course of the 3rd quarter of the corporate’s 2022 fiscal 12 months. For the primary 9 months of the 12 months as a complete, income got here in at $1.64 billion. This represents a 42.1% building up over the $1.15 billion generated the similar time final 12 months. Maximum of this enlargement got here from the corporate’s North American operations, with gross sales leaping via 34.7% from $989.7 million to $1.33 billion. On a share foundation even though, the true enlargement got here from its presence in Europe, with gross sales skyrocketing 90.7% from $155.6 million to $296.6 million. Such fast enlargement is never the results of natural actions. However that is a kind of uncommon exceptions the place that’s the case. From 2021 via lately, the company has raised costs 4 separate occasions to offset emerging uncooked subject matter prices. The company additionally benefited to the track of $147.8 million from its acquisition of ETANCO.

With this upward thrust in income, we additionally noticed stepped forward profitability. Internet source of revenue for the corporate rose from $196.7 million to $276.4 million. This got here at a time when gross margins for the corporate in fact worsened, losing from 48.2% to 45.1%, in large part because of its aforementioned acquisition. Different profitability metrics adopted a equivalent trajectory. Working money waft shot up from $122.1 million to $263.4 million. If we regulate for adjustments in operating capital, it nonetheless would have risen from $254 million to $339 million. In the meantime, even EBITDA for the corporate stepped forward, emerging from $303.8 million to $450.5 million.

Writer – SEC EDGAR Knowledge

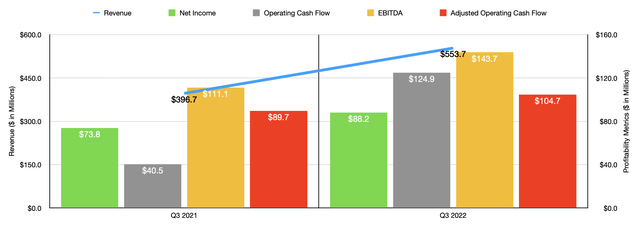

Clearly, effects for the year-to-date length are certainly necessary. On the other hand, we additionally want to be aware of the latest knowledge by itself. In spite of everything, we’re coping with converting financial stipulations. Fortunately, within the 3rd quarter by itself, the company has achieved somewhat neatly, with income of $553.7 million dwarfing the $396.7 million reported 12 months previous. The similar components that impacted the year-to-date effects for the corporate have additionally impacted, in a good manner, the corporate’s effects for the 3rd quarter. In the meantime, profitability figures for the corporate proceed to support. Internet source of revenue rose from $73.8 million to $88.2 million. As soon as once more, the gross margin for the corporate suffered, falling from 49.9% to 44.2%, with a lot of that because of the aforementioned acquisition. On the identical time, working money waft greater than tripled from $40.5 million to $124.9 million. If we regulate for adjustments in operating capital, it could have risen from $89.7 million to $104.7 million. Even EBITDA remained on the upward thrust, mountaineering from $111.1 million to $143.7 million.

Writer – SEC EDGAR Knowledge

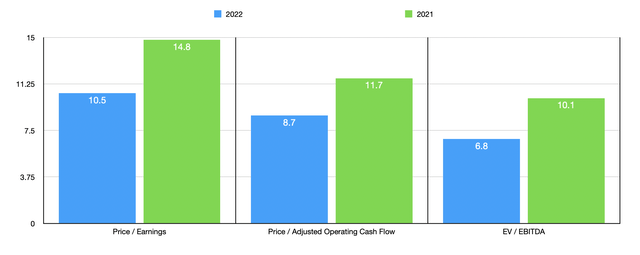

Even though control has equipped some ideas on how 2022 as a complete may finally end up, we do not in reality have a lot to move on that may be of worth. As a substitute, if we simply annualize effects skilled thus far for the 12 months, we might get internet source of revenue of $374.3 million, adjusted working money waft of $450.8 million, and EBITDA of $634.7 million. Those numbers would suggest a ahead payment to revenue a couple of of 10.5, a ahead payment to adjusted working money waft a couple of of 8.7, and a ahead EV to EBITDA a couple of of 6.8. Even though effects revert again to what we noticed in 2021, those multiples would no longer be unreasonable, coming in at 14.8, 11.7, and 10.1, respectively. Once I final wrote concerning the corporate, the knowledge for the 2021 fiscal 12 months implied multiples of 18.4, 14.5, and 10.7, respectively. So in two of the 3 manners, stocks have got meaningfully inexpensive. As a part of my research, I additionally when put next the corporate to 5 equivalent corporations. On a price-to-earnings foundation, the firms ranged from a low of three.9 to a prime of 18. On this case, 3 of the 5 had been inexpensive than our prospect. The use of the associated fee to working money waft manner, the variety is from 3.2 to twenty.9, with two of the 5 corporations being inexpensive than our goal. And on the subject of the EV to EBITDA manner, the variety is between 2.8 and 11.5. On this state of affairs, 4 of the 5 are inexpensive than our prospect.

| Corporate | Worth / Profits | Worth / Working Money Float | EV / EBITDA |

| Simpson Production | 10.5 | 8.7 | 6.8 |

| Developers FirstSource (BLDR) | 3.9 | 3.2 | 2.8 |

| Armstrong International Industries (AWI) | 18.0 | 20.9 | 11.5 |

| Tecnoglass (TGLS) | 11.2 | 11.6 | 6.7 |

| Owens Corning (OC) | 6.6 | 6.2 | 4.5 |

| UFP Industries (UFPI) | 7.0 | 6.1 | 4.4 |

Takeaway

What we’ve to be had to us lately is an organization this is buying and selling at the reasonable on an absolute foundation however in a variety this is very similar to its friends. In the future, monetary efficiency more than likely will weaken, particularly if rates of interest have the affect that we think them to. The corporate is reinforced via the truth that it has no debt and has money available of $301.2 million. That gives quite a lot of flexibility and coverage for shareholders. Total, I’d say that the danger of an everlasting lack of capital for shareholders could be very low. However I would not be stunned, given marketplace stipulations, of possibly some transient ache. Given how reasonable the inventory is presently even though, it’s getting moderately tempting. But if factoring within the financial considerations, I do assume it nonetheless makes extra sense as a ‘grasp’ for now. But when the image will get any further favorable for traders, that score may alternate.

https://seekingalpha.com/article/4559252-simpson-manufacturing-nearing-an-inflection-point