Chris McGrath/Getty Photographs Information

Via Robert Hughes

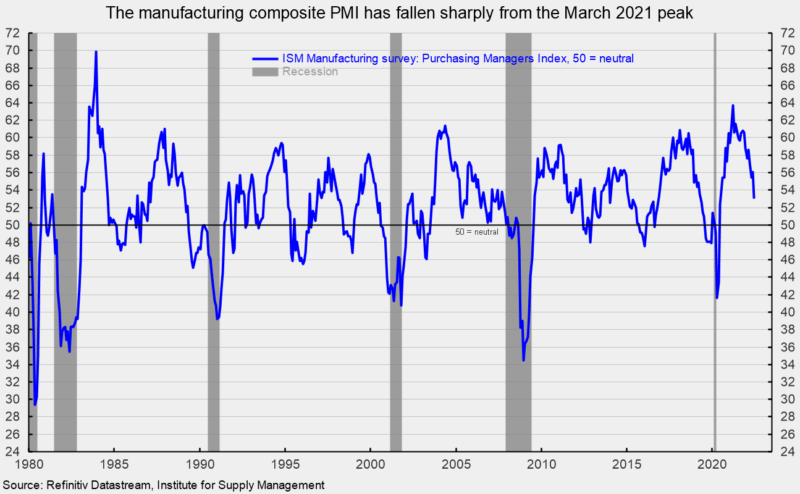

The Institute for Provide Control’s Production Buying Managers’ Index fell to 53.0 p.c in June, off 3.1 issues from 56.1 p.c in Would possibly (50 is impartial). June is the twenty fifth consecutive studying above the impartial threshold, however the degree is down sharply from the March 2021 top (see first chart). The survey effects point out that the producing sector continues to increase, however call for has softened, and worth pressures have eased barely, although they remained important. On the other hand, survey respondents remained positive about long run call for.

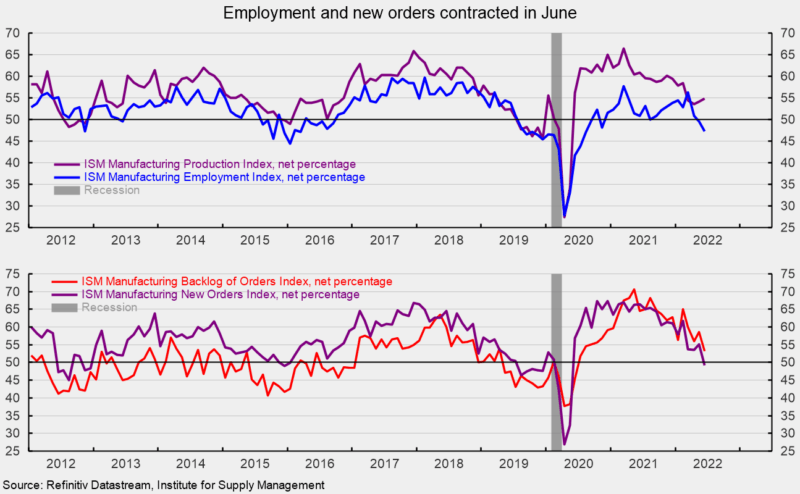

The Manufacturing Index registered a 54.9 p.c lead to June, a upward thrust of 0.7 issues from Would possibly (see most sensible of 2d chart). The index has been above 50 for 25 months, however the six-month reasonable has declined for 15 consecutive months and the June reasonable of 55.6 p.c is the bottom since September 2020.

The Employment Index posted a 3rd consecutive decline in June, coming in underneath the impartial 50 threshold for the second one consecutive month. The 47.3 p.c studying suggests two months of contracting employment (see most sensible of 2d chart). The record states, “Regardless of the Employment Index contracting in Would possibly and June, firms stepped forward their development on addressing moderate-term hard work shortages in any respect tiers of the provision chain, in line with Trade Survey Committee respondents’ feedback. Panelists reported decrease charges of quits in comparison to Would possibly.”

The Bureau of Hard work Statistics’ Employment State of affairs record for June is due out on Friday, July 8, and expectancies are for a achieve of 265,000 nonfarm payroll jobs together with the addition of 12,000 jobs in production.

The brand new orders index sank 5.9 issues to 49.2 p.c in June. That’s the first studying underneath impartial since Would possibly 2020 (see backside of 2d chart). The brand new export orders index, a separate measure from new orders, fell to 50.7 p.c as opposed to 52.9 p.c in Would possibly. The brand new export orders index has been above 50 for twenty-four consecutive months.

The Backlog-of-Orders Index got here in at 53.2 p.c as opposed to 58.7 p.c in Would possibly, a 5.5-point decline (see backside of 2d chart). This measure has pulled again from the record-high 70.6 p.c lead to Would possibly 2021 however has been above 50 for twenty-four consecutive months. The index suggests producers’ backlogs proceed to upward thrust, however the tempo decelerated considerably in contemporary months.

Buyer inventories in June are nonetheless regarded as too low, with the index coming in at 35.2 p.c, up 2.5 issues from Would possibly (index effects underneath 50 point out consumers’ inventories are too low). The index has been underneath 50 for 69 consecutive months. Inadequate stock is a good signal for long run manufacturing.

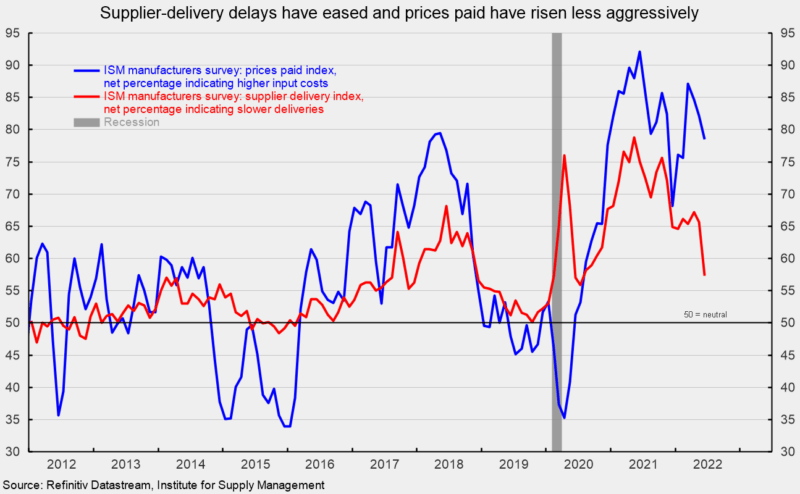

The index for costs for enter fabrics eased again for the 3rd consecutive month in June, falling 3.7 issues to 78.5 p.c (see 3rd chart). The index is down from 87.1 p.c in March 2022 and suggests payment pressures, although nonetheless intense, have eased barely.

The provider deliveries index registered a 57.3 p.c lead to June, down 8.4 issues from the Would possibly consequence. The index used to be at 78.8 p.c in Would possibly 2021. The declines over the last yr recommend deliveries are slowing at a far slower fee (see 3rd chart).

General, production survey respondents remained positive that wholesome call for will proceed. Noticeable softening amongst a number of person survey indexes suggests provide and insist could also be transferring nearer to stability, serving to ease some upward payment pressures. Moreover, at the provide aspect, fallout from the Russian warfare towards Ukraine continues to disrupt world provide chains. At the call for aspect, constantly increased payment will increase are impacting client call for and an intensifying Fed coverage tightening cycle is boosting financing prices. The outlook stays extremely unsure.

Editor’s Notice: The abstract bullets for this text have been selected through Looking for Alpha editors.

https://seekingalpha.com/article/4521420-manufacturing-sector-survey-suggests-slowing-growth-and-slightly-fewer-price-pressures